China’s high-speed railways plunge from high profits into a debt trap

Just over a decade ago, in 2009, China’s first long-distance high-speed rail (HSR) service covered the 968 kilometers between

Wuhan and Guangzhou at an average speed of around 350 kilometres per hour. The feat was recognised as the Communist Party of China’s “

debt-fuelled” response to the global financial crisis. It was a sort of a “Railway Keynesianism,” where China re-engineered its railway infrastructure to drive the demand for concrete and steel and create millions of jobs. In the decade that followed, China’s HSR network spanned over a

track length of 38,000 kilometres, the highest in the world. Bagging a share of 26 percent of the country’s total railway network, HSR today connects almost every major city in China, with travel time just a couple of hours more than air travel, but with the comfort that only trains can provide.

China’s HSR obsession

In the mad rush to gain the rich economic dividends that the HSR delivered on several profitable lines, especially the

Beijing-Shanghai and Beijing-Guangzhou lines, provincial governments across the country have blindly tried to

emulate the feat. However, most of such provincial construction has ignored the low- to zero- potential of the expensive routes to attract similar volumes of passenger traffic and are running at high idle capacity.

Most new HSR lines in China have witnessed a sharp decline in their “transportation density”. Measured in passenger-kilometres, it is an indicator that projects the line’s operating efficiency in terms of annual average transport volume per kilometre. For example, while the 1,318-kilometre

Beijing-Shanghai HSR corridor’s transportation density was 48 million passenger-kilometres in 2015 and continues to be high, the 1,776-kilometre Lanzhou-Urumqi line has only 2.3 million passenger-kilometres of transportation density. China’s overall transportation density of HSR was 17 million passenger-kilometres in 2015, while it was

34 million passenger-kilometres for Japan’s Shinkansen in the same year.

Most new HSR lines in China have witnessed a sharp decline in their “transportation density”. Measured in passenger-kilometres, it is an indicator that projects the line’s operating efficiency in terms of annual average transport volume per kilometre

HSR construction costs nearly

three times more than a conventional rail line. Given the absence of freight tariffs, its operational viability is hinged solely on passenger fares to cover the capital expenditure and operating costs. The craze for HSR has made China neglect the construction of conventional systems, adversely affecting the balance of the country’s logistics mix. As a result, rail has consistently

trailed road and water freight transport for the past several years. This has led to growing investments in polluting freight road trucks and trailers,

offsetting the environmental gains resulting from HSR. But for the China Rail Corporation (CRC) that owns the HSR network, that is the least of its worries.

Entangled in an HSR debt trap

In the past few years, mega borrowings by provincial governments to monetise its HSR lines have created a

debt trap, which is now pinching the coffers of the state-owned CRC. CRC’s financial woes started nearly four years ago when more than 60 percent of the HSR operators each lost a minimum of US $100 million in 2018. That year, the least profitable operator in Chengdu reported

net loss of US $1.8 billion. In the same year, transport economists in China had predicted an

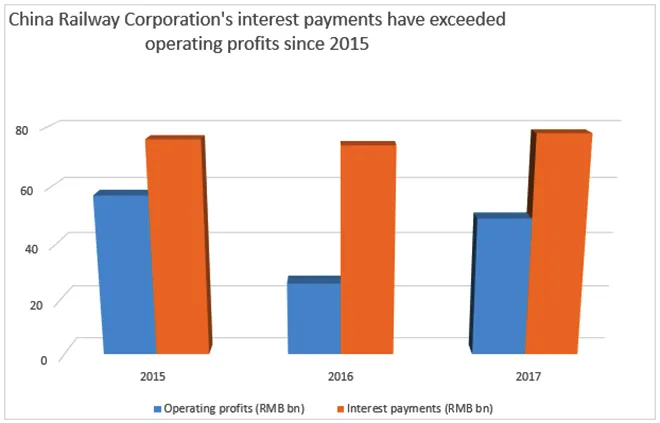

impending debt crisis for the country’s HSR that was dependent on “unsustainable government subsidies with many lines incapable of repaying the interest on their debt, let alone principal”, and were caught in a vicious cycle of “raising new debt to pay off old debt”. Consequently, since 2015, CRC’s interest payments have been significantly higher than its operating profits, shrinking its bottom line.

Source:

Source: China Railways and

Financial Times

Four years later, in March 2021, China’s State Council, the highest organ of state power, has waved a red flag to

curtail investments in HSR to prevent the slide into a deepening debt trap. The new guidelines have stopped the construction of new HSR corridors, primarily on underutilised routes that are operating at less than 80 percent of prescribed capacity. For China, which has seen the length of its high-speed railway network

increase by 91 percent between 2015 and 2020, the new guidelines indicate that the country’s pursuit for speed has come at a high price.

For China, which has seen the length of its high-speed railway network increase by 91 percent between 2015 and 2020, the new guidelines indicate that the country’s pursuit for speed has come at a high price.

Without mentioning a specific figure or even a range, the State Council has asked all governments to ensure that their railway debts should be within a “

rational range” by 2035. In September 2020, CRC’s

quantum of debt rose to RMB 5.57 trillion (US $850 billion) – up from RMB 5.28 trillion as of September 2019, catapulting its debt-to-asset ratio to 65.8 percent.

The guidelines have asked governments to avoid blind competition, obsolete and redundant construction, and “improve the early-warning mechanism over railway-related debt.” It has suspended all construction in regions where the debt burden is high and surpasses its fiscal strength. Debt-ridden cities building underground or light railway systems too have been suspended.

Within just three days of the guidelines being released, Beijing

stopped work on two HSR projects worth over RMB 130 billion (US $20 billion) in Shandong and Shaanxi provinces. Shandong’s 270-kilometre line had sought to connect its capital Jinan with its southern city of Zaozhuang. Shandong was also ordered to stop work on the RMB 71.6 billion Guanzhong Chengji project, which consists of 13 lines in Northwest China’s Shaanxi. A

post on the Shaanxi government website informed that the project has been stopped to “lower risk levels”, following an integrated review of the situation regarding rail construction and finances.

The increased heat on the debt-riddled operators has also dented the bottom lines of the investment banks and the shareholders of China’s Railway Development Fund (RDF). As bond yields nosedived and profits crashed, the CRC has decided to

liquidate RDF nine years early to avoid paying dividends to the investors. Set up in 2014 to raise money for China’s growing HSR network, the RDF offered preferred shares with steady returns to investors. A

fixed annual return of 5.5 percent was offered to the first four banks that invested in RDF, while investor banks that came later were promised 5.32 percent returns. Reeling under a record loss of RMB 61.4 billion in the first quarter of 2020 as a result of a 54.8 percent year-on-year crash in passenger earnings owing to the pandemic-induced restrictions on travel, the CRC has found it difficult to pay such high assured returns. To make matters more unpleasant for the investors, the interest rates on the nine 20-year bonds issued by RDF

crashed from a high of 5.78 percent in 2014 to an all-time low of 3.97 percent in 2020.

India must be cautious

China’s HSR story has dazzled the world in the past decade. But its growing domestic financial woes have exposed its risky underbelly. Poorer countries trying to emulate HSR must be mindful of the pitfalls

China’s HSR story has dazzled the world in the past decade. But its growing domestic financial woes have exposed its risky underbelly. Poorer countries trying to emulate HSR must be mindful of the pitfalls. India, which is expected to start trial runs over a short distance of its much-touted Mumbai–Ahmedabad HSR project in 2024, must be extra careful. The work on the INR 1.08 trillion (US $14.3 billion) project has already been

delayed by five years from 2023 to 2028. The Japan International Cooperation Agency (JICA)–funded project will traverse a distance of 508 kilometres with the

construction cost of the rail infrastructure being pegged at US $27.44 million per kilometre, closer to the higher European HSR standard. In comparison, China’s HSR costs an average of up to US $21 million per kilometre. India, with a per capita income of US $1,709, must also consider that China and Japan, its two Asian counterparts with HSR, have per capita incomes of nearly US $8,123 and US $38,895 respectively. The affordability factor may play a critical role in India achieving sustainable transportation density and also could prove to be its biggest weakness.

Just over a decade ago, in 2009, China’s first long-distance high-speed rail (HSR) service covered the 968 kilometers between

Wuhan and Guangzhou at an average speed of around 350 kilometres per hour. The feat was recognised as the Communist Party of China’s “

debt-fuelled” response to the global financial crisis. It was a sort of a “Railway Keynesianism,” where China re-engineered its railway infrastructure to drive the demand for concrete and steel and create millions of jobs. In the decade that followed, China’s HSR network spanned over a

track length of 38,000 kilometres, the highest in the world. Bagging a share of 26 percent of the country’s total railway network, HSR today connects almost every major city in China, with travel time just a couple of hours more than air travel, but with the comfort that only trains can provide.

China’s HSR obsession

In the mad rush to gain the rich economic dividends that the HSR delivered on several profitable lines, especially the

Beijing-Shanghai and Beijing-Guangzhou lines, provincial governments across the country have blindly tried to

emulate the feat. However, most of such provincial construction has ignored the low- to zero- potential of the expensive routes to attract similar volumes of passenger traffic and are running at high idle capacity.

Most new HSR lines in China have witnessed a sharp decline in their “transportation density”. Measured in passenger-kilometres, it is an indicator that projects the line’s operating efficiency in terms of annual average transport volume per kilometre. For example, while the 1,318-kilometre

Beijing-Shanghai HSR corridor’s transportation density was 48 million passenger-kilometres in 2015 and continues to be high, the 1,776-kilometre Lanzhou-Urumqi line has only 2.3 million passenger-kilometres of transportation density. China’s overall transportation density of HSR was 17 million passenger-kilometres in 2015, while it was

34 million passenger-kilometres for Japan’s Shinkansen in the same year.

Most new HSR lines in China have witnessed a sharp decline in their “transportation density”. Measured in passenger-kilometres, it is an indicator that projects the line’s operating efficiency in terms of annual average transport volume per kilometre

HSR construction costs nearly

three times more than a conventional rail line. Given the absence of freight tariffs, its operational viability is hinged solely on passenger fares to cover the capital expenditure and operating costs. The craze for HSR has made China neglect the construction of conventional systems, adversely affecting the balance of the country’s logistics mix. As a result, rail has consistently

trailed road and water freight transport for the past several years. This has led to growing investments in polluting freight road trucks and trailers,

offsetting the environmental gains resulting from HSR. But for the China Rail Corporation (CRC) that owns the HSR network, that is the least of its worries.

Entangled in an HSR debt trap

In the past few years, mega borrowings by provincial governments to monetise its HSR lines have created a

debt trap, which is now pinching the coffers of the state-owned CRC. CRC’s financial woes started nearly four years ago when more than 60 percent of the HSR operators each lost a minimum of US $100 million in 2018. That year, the least profitable operator in Chengdu reported

net loss of US $1.8 billion. In the same year, transport economists in China had predicted an

impending debt crisis for the country’s HSR that was dependent on “unsustainable government subsidies with many lines incapable of repaying the interest on their debt, let alone principal”, and were caught in a vicious cycle of “raising new debt to pay off old debt”. Consequently, since 2015, CRC’s interest payments have been significantly higher than its operating profits, shrinking its bottom line.

Source: China Railways and

Financial Times

Four years later, in March 2021, China’s State Council, the highest organ of state power, has waved a red flag to

curtail investments in HSR to prevent the slide into a deepening debt trap. The new guidelines have stopped the construction of new HSR corridors, primarily on underutilised routes that are operating at less than 80 percent of prescribed capacity. For China, which has seen the length of its high-speed railway network

increase by 91 percent between 2015 and 2020, the new guidelines indicate that the country’s pursuit for speed has come at a high price.

For China, which has seen the length of its high-speed railway network increase by 91 percent between 2015 and 2020, the new guidelines indicate that the country’s pursuit for speed has come at a high price.

Without mentioning a specific figure or even a range, the State Council has asked all governments to ensure that their railway debts should be within a “

rational range” by 2035. In September 2020, CRC’s

quantum of debt rose to RMB 5.57 trillion (US $850 billion) – up from RMB 5.28 trillion as of September 2019, catapulting its debt-to-asset ratio to 65.8 percent.

The guidelines have asked governments to avoid blind competition, obsolete and redundant construction, and “improve the early-warning mechanism over railway-related debt.” It has suspended all construction in regions where the debt burden is high and surpasses its fiscal strength. Debt-ridden cities building underground or light railway systems too have been suspended.

Within just three days of the guidelines being released, Beijing

stopped work on two HSR projects worth over RMB 130 billion (US $20 billion) in Shandong and Shaanxi provinces. Shandong’s 270-kilometre line had sought to connect its capital Jinan with its southern city of Zaozhuang. Shandong was also ordered to stop work on the RMB 71.6 billion Guanzhong Chengji project, which consists of 13 lines in Northwest China’s Shaanxi. A

post on the Shaanxi government website informed that the project has been stopped to “lower risk levels”, following an integrated review of the situation regarding rail construction and finances.

The increased heat on the debt-riddled operators has also dented the bottom lines of the investment banks and the shareholders of China’s Railway Development Fund (RDF). As bond yields nosedived and profits crashed, the CRC has decided to

liquidate RDF nine years early to avoid paying dividends to the investors. Set up in 2014 to raise money for China’s growing HSR network, the RDF offered preferred shares with steady returns to investors. A

fixed annual return of 5.5 percent was offered to the first four banks that invested in RDF, while investor banks that came later were promised 5.32 percent returns. Reeling under a record loss of RMB 61.4 billion in the first quarter of 2020 as a result of a 54.8 percent year-on-year crash in passenger earnings owing to the pandemic-induced restrictions on travel, the CRC has found it difficult to pay such high assured returns. To make matters more unpleasant for the investors, the interest rates on the nine 20-year bonds issued by RDF

crashed from a high of 5.78 percent in 2014 to an all-time low of 3.97 percent in 2020.

India must be cautious

China’s HSR story has dazzled the world in the past decade. But its growing domestic financial woes have exposed its risky underbelly. Poorer countries trying to emulate HSR must be mindful of the pitfalls

China’s HSR story has dazzled the world in the past decade. But its growing domestic financial woes have exposed its risky underbelly. Poorer countries trying to emulate HSR must be mindful of the pitfalls. India, which is expected to start trial runs over a short distance of its much-touted Mumbai–Ahmedabad HSR project in 2024, must be extra careful. The work on the INR 1.08 trillion (US $14.3 billion) project has already been

delayed by five years from 2023 to 2028. The Japan International Cooperation Agency (JICA)–funded project will traverse a distance of 508 kilometres with the

construction cost of the rail infrastructure being pegged at US $27.44 million per kilometre, closer to the higher European HSR standard. In comparison, China’s HSR costs an average of up to US $21 million per kilometre. India, with a per capita income of US $1,709, must also consider that China and Japan, its two Asian counterparts with HSR, have per capita incomes of nearly US $8,123 and US $38,895 respectively. The affordability factor may play a critical role in India achieving sustainable transportation density and also could prove to be its biggest weakness.

Most new HSR lines in China have witnessed a sharp decline in their “transportation density”. Measured in passenger-kilometres

www-orfonline-org.cdn.ampproject.org

www.bloomberg.com

www.bloomberg.com